Paying for Dirt: Where Have home values detached from construction costs?

Source: http://www.oregonmetro.gov

In the expensive U.S. coastal metros, home prices have detached from construction costs and can be almost four times as high as the cost of rebuilding existing structures. However, absent restrictions on housing supply, competition among developers tends to maintain average metropolitan home prices tethered to the cost of construction.

This study estimates the average home value to replacement cost ratio for the largest U.S. metro areas, as well as several related measures, and maps them by zip code area within each metro.

The high cost of housing in expensive coastal metros is not driven by construction costs. It is driven by the high cost of land which, in turn, reflects a scarcity of zoned units, not a scarcity of land per se.

The scarcity of zoned units afflicts the expensive coastal metros in their entirety but, even within more affordable metro areas, sought-after districts suffer from such scarcity.

The disconnect between home values and construction costs in the expensive coastal metros does not imply that real estate development is necessarily lucrative. Because developers must acquire valuable land, construction costs can still be pivotal with respect to the viability of projects and, as a result, they can still influence the housing supply. The timing of developers’ land acquisition vis-a-vis the housing cycle can be crucial.

Anyone who has seen a million dollar bungalow can attest that, in America’s expensive coastal cities, the disparity between a home’s appearance and its price tag can be shocking. Real estate property values consist of two parts: the value of land and the value of improvements to it, like structures. In the expensive coastal cities, the land component corresponds first and foremost to a premium paid for staking a claim in the location, and it can be huge, generally comprising most of a home’s value.

This study illustrates the disparity between the appearance and price tag of homes, identifying the places in which home buyers pay mostly for the dirt. For each of the largest U.S. metros – and for each zip code area therein – it estimates average home values and replacement costs: the cost of building existing homes anew at current quality standards and construction costs. The estimates help infer the breakdown of home value between the value of improvements – primarily the structure – and the value of the land. Sources and methodology are detailed in the appendix, and the complete set of estimates is available for download.

Construction costs differ from place to place, but they pale in comparison to the differences in home prices

The differences across metros in construction costs are not negligible. Even though the cost of building materials varies relatively little from place to place, construction requires labor whose wages vary more substantially across metros. In addition, the typical size and quality of homes are not the same from place to place. This means that, even if an identical home layout costs the same to build in two places, actual costs will differ if one metro sprouts single-family mansions while the other builds modest apartments.

However, the differences in construction costs across metros pale in comparison to those in home values. The following chart compares U.S. metros’ average home values with the average replacement cost of existing homes. As of 2016, the San Jose metro area had the highest average home value, at $1,133,000, and the Buffalo metro area had the lowest, at $167,000 – an almost seven-fold difference. In contrast, the San Francisco metro area had the highest per-unit replacement cost at $338,000 and the Las Vegas metro area had the lowest at $157,000 – different only by about a factor of two. Even if we exclude the coastal California metros – whose average home values are the highest in the nation and which account for the four highest points in the chart – home values still differ by a factor of more than 3.3 between the most and least expensive metros compared to a factor of 1.8 for replacement costs.

Thus, construction costs probably aren’t driving the differences in home values across metros. Rather, home values – which depend on the number of homes available and on people’s willingness to pay for them – include vastly different land value components.

Why does the cost of construction matter?

Construction costs influence developers’ decisions about whether to build and what to build and, in turn, these decisions determine how the housing supply – and home prices – evolve. First of all, profit-seeking developers won’t build homes whose construction cost exceeds their expected sale value. As a result – even though estimated metro averages are just rough approximations that mask a great deal of diversity – metros with an average home value below the average replacement cost are unlikely to see large amounts of new construction.

On the other hand, if the demand for housing is sufficient that developers expect to recoup costs and turn a profit, they opt to build, and competition among them keeps new home prices loosely tethered to the cost of producing them. The catch is that producing homes costs more than just the cost of construction: it also requires financing, operational overhead, regulatory fees and – potentially dominating all others expenses – the acquisition of land. When opportunities for construction abound, i.e. when land is fairly inexpensive, competing developers tend to build enough new housing to drive down home values, maintaining them close to the cost of construction.

However, when opportunities for construction are more limited – because either land or the number of units allowed to be built upon it are scarce relative to demand – land grows expensive and developers build fewer homes than they would otherwise (their projects then cater to more affluent buyers, too). As a result, the land value component grows and home values, no longer tethered to the cost of construction, can soar as high as people are willing to pay.

The logic put forth here is not just theoretical, it is consistent with the data. The chart below shows the average relationship between the home value to replacement cost ratio, observed in 2016, and the amount of new home construction between 2000 and 2016 (so no, X does not cause Y here). On the left, e.g. in the Detroit metro area, the average home value is below the average replacement cost, suggesting it is unlikely for new construction to be viable and keeping its rate low (Detroit’s ratio was roughly similar in the year 2000 as well). In the middle are metro areas like Chicago and Atlanta, which offer a relative abundance of opportunities to build. Despite the abundance, not all of these metros see high rates of new construction, as Chicago and Atlanta demonstrate, because they differ in their economic vitality and consequently in their draw on people. However, on average, they experience high rates of home construction which keep home values modest and prevent the home value to replacement cost ratio from rising. Finally, on the right are the expensive coastal metros – San Jose and San Francisco being the most extreme – with strong economies and a restricted set of opportunities to build, which limits the rate of home construction and raises home values. Because home values in the expensive coastal metros are vastly different than elsewhere but construction costs are not, these metros’ home value to replacement cost ratios are high as well.

Where do people pay the largest premium for land?

The following chart ranks the largest U.S. metro areas according to the ratio of home value to replacement cost, a rough gauge of the extent to which home values are driven by the value of land. When home values are much greater than replacement costs it means they derive mostly from land, but when they are similar to replacement costs, it means they derive more heavily from the value of improvements. Home values can also fall below the cost of replacement, i.e. the ratio can drop below one. This occurs when land is very cheap, homes are in a poor state of repair, or both (to see why, recall that home values are the sum of land and improvement values, and consider that improvement values are almost always below replacement costs, because homes are in less than mint condition). The interactive chart below allows the reader to rank metros by additional measures – please explore!

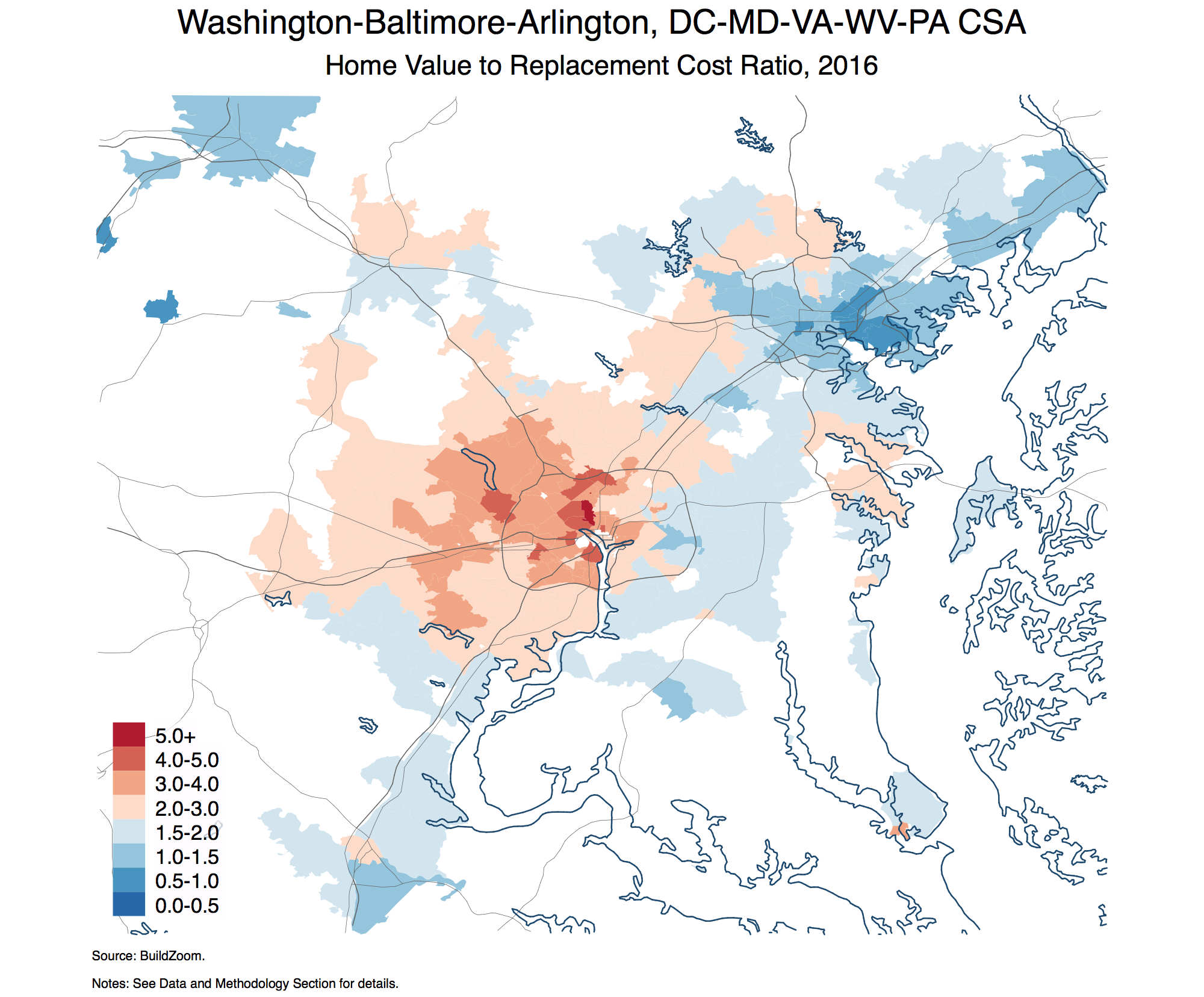

In the expensive coastal metros, home values greatly exceed the cost of replacement. The San Jose metro area – Silicon Valley – tops the chart with a ratio of 3.74, followed by the San Francisco metro area with a ratio of 2.98 and the Washington, New York, and Los Angeles metros with ratios of 2.63, 2.62 and 2.53.

The numbers indicate that, in these coastal metros, the value of homes derives far less from their material presence than it does from the opportunity they offer for living and working in the metro. Since the 1970s these metros have gradually slowed their outward expansion in an effort to stem sprawl but, failing to compensate by growing denser inside the developed footprint, they also stunted their housing production. Yet, even as they restricted their supply of housing, these metros’ intense draw on people did not abate and, as a result, home prices diverged from the cost of construction, creating the thick wedge of inflated land values that exists there today.

In contrast, home values in rust belt metros such as Detroit and Buffalo, whose economic base has eroded and which I have dubbed elsewhere as legacy cities, are well below the cost of replacement. Detroit’s home value to replacement cost ratio is 0.81 and Buffalo’s is 0.74. When homes are valued below the replacement cost, it means that they wouldn’t be financially viable to build today. Some legacy cities – notably Pittsburgh – stand out for substantial increases in home values in recent years, yet they have an abundance of legacy housing which has so far prevented their home values from rising sufficiently to justify large amounts of new construction.

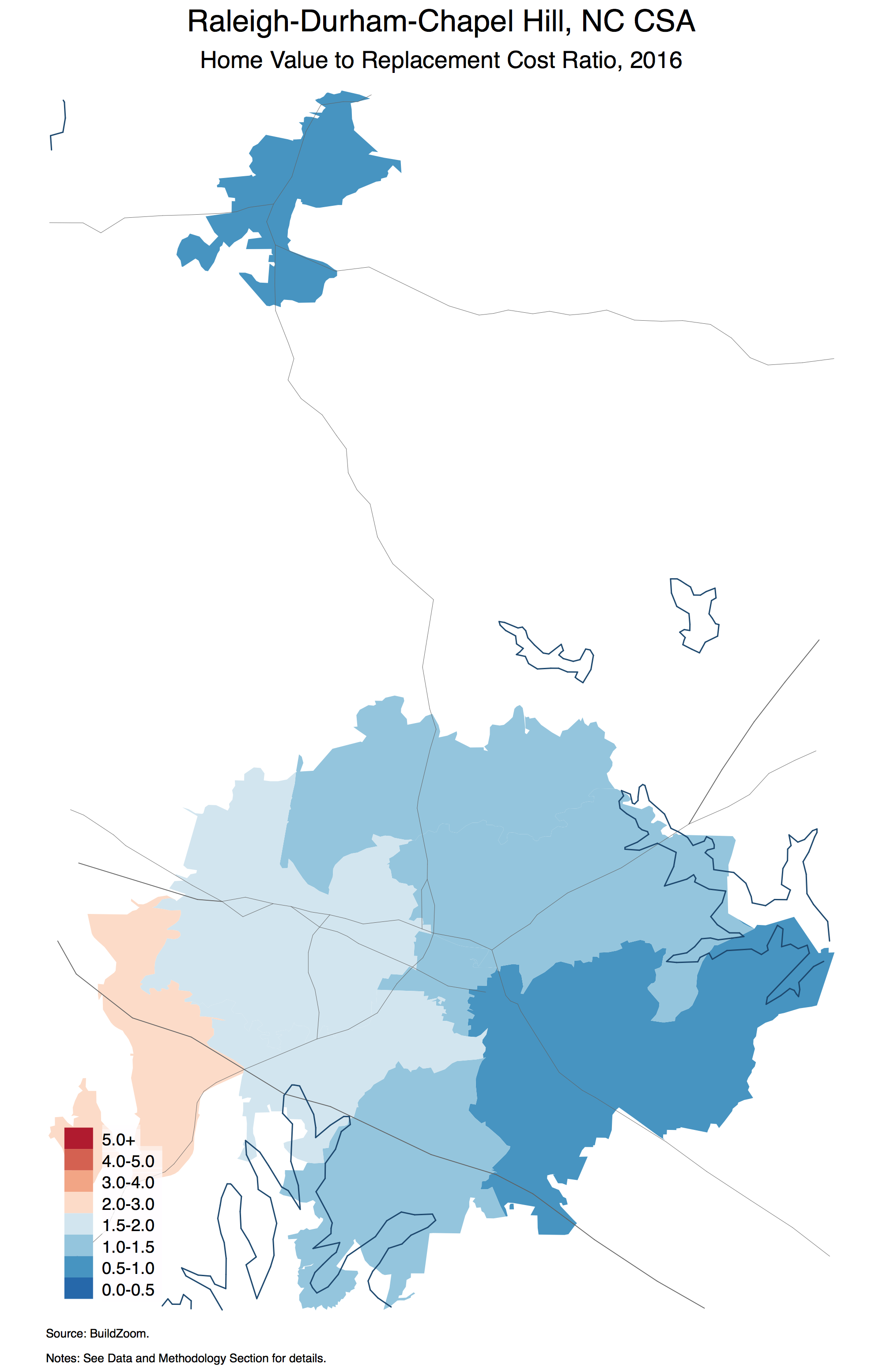

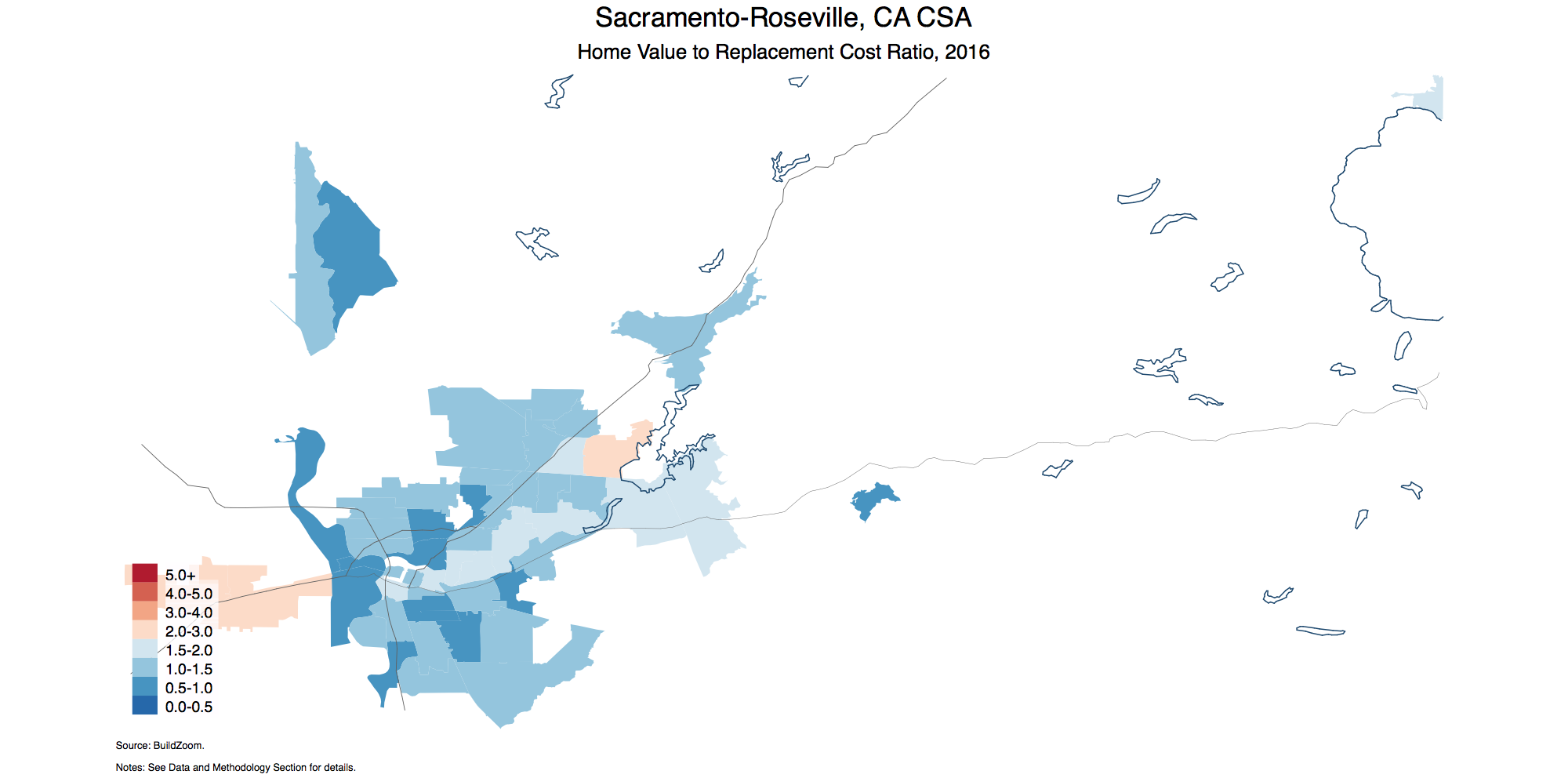

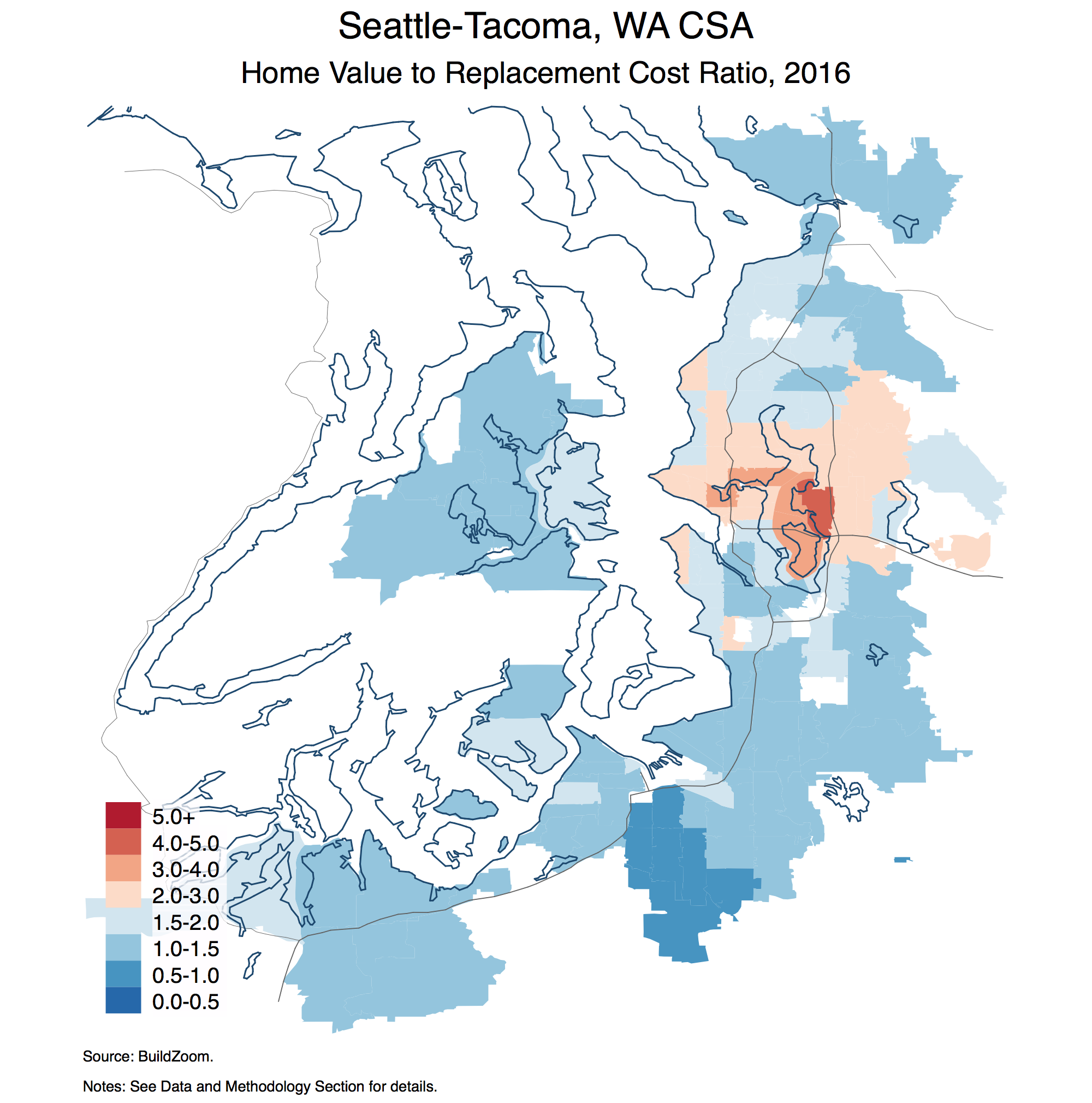

However, most metro areas inhabit the broad middle of the chart. Metros in the 1 to 1.5 range, such as Atlanta (1.38), Charlotte (1.16), and Dallas (1.12), have produced sufficient amounts of new housing over the years to maintain home values relatively near the cost of construction. I refer to these metros as expansive cities because they have done so almost exclusively by expanding outward, i.e. consuming ever more land as opposed to using it more efficiently by growing denser. The 1.5 to 2 range contains metros like Denver (1.77), Portland (1.66), and Seattle (1.80). Their level of disparity between home values and replacement costs is not as extreme as in some of the expensive coastal cities, but they are nevertheless experiencing reduced affordability.

Even in metros that supply abundant new housing, homes in key locations are meted out

Some metros, like Atlanta (1.38) and Houston (1.54) have in recent years produced some the largest percent increases in housing stock of any U.S. metro. However, despite producing abundant new housing, they are failing to produce enough new homes to suppress appreciation in specific sought-after areas. Such sought-after areas are typically located in the metro’s interior, and their housing supply can only grow through densification. This pattern affects all U.S. metros to some extent, reflecting the broader shift towards placing greater value on central urban location, but in metros whose home value to replacement cost ratio is higher the pattern is more advanced.

Despite being the poster-children of the expansive growth pattern, the stretches of affluence in western Houston and northern Atlanta exhibit home values at least 3 times as high as the replacement cost.

How can this be? Even though expansive metros offer an abundance of housing globally, the supply of housing in sought-after areas within the metro is often locally limited. Prices in areas that are closer to the metropolitan fringe can be suppressed by growth on nearby vacant land – of which leapfrog development leaves plenty – but areas deeper in the interior tend to be “landlocked.” Local land use regulation typically prevents suburban fabric from growing denser and, as a result, “landlocked” interior areas can only add housing on a finite number of vacant lots, which are gradually depleted. When people are willing to pay well above construction costs to live in sought-after areas in the interior and don’t view the abundant housing elsewhere in the metro as a sufficiently attractive substitute, these areas can experience land value inflation, too.

In contrast, home values in expensive coastal metros tend to be much higher than replacement cost even very far from the center. This is because the supply of housing in such metros is globally restricted. The San Francisco Bay Area is the most acute example, with low home value to replacement cost ratios almost nowhere to be found. In the Los Angeles metro area, lower land value components can be found mostly in the so-called “Inland Empire” to the east, and in the New York metro area one has to travel a great distance from Manhattan to find such areas.

On average, one has to go 30-40 miles out from the center of an expensive coastal city to drop below a home value to replacement cost ratio of two. Even beyond the 50 mile mark, the ratio is closer to two than to one. In more affordable expansive cities, on the other hand, home values tend towards replacement costs near the metropolitan fringe because land there is relatively inexpensive. In most of such metros, one only has to go 5 miles out from the center to reach areas with home value to replacement cost ratios below 2, and at the fringe the ratio is essentially one.

When home buyers are paying for dirt, someone is being excluded, and the solution is to densify

High home value to replacement cost ratios are a good indication that the housing supply is restricted, meaning that people who are willing and able to pay enough to support new housing construction are being excluded by limits on density.

Both expensive coastal metros and affordable expansive ones would benefit from the relaxation of restrictions on housing density, but for slightly different reasons. Whereas the former need greater housing density to combat a full-blown housing affordability crisis, the latter need it in order wean off sprawl without creating an affordability crisis of their own.

Doesn’t upzoning just raise the value of land?

A common objection to increasing a lot’s permitted housing density or – loosely speaking – upzoning it, is that it simply raises the value of the land in reaction to the increase in density rather than resulting in cheaper homes. Although there is truth to the observation, it is a poor argument against raising density. When upzoning raises land values it indicates that the scarce factor drawing a premium is not land per se, but the units zoned upon it. It is mistaken to think that upzoning will reduce the land value component of homes simply by dividing a fixed land value over a greater number of units. The value of land depends on its characteristics, one of which is the number of units it is zoned for – i.e. the number of households allowed to call it home – and changing that number affects the land’s value. But upzoning also increases the number of zoned units in the housing market as a whole, and in so doing will contribute to easing their scarcity.

For upzoning to meaningfully suppress housing prices, it must be applied en masse. Upzoning a limited number of lots – where “limited” means small compared to the relevant housing market – will raise the value of the upzoned land without measurably influencing home values. To suppress housing prices, upzoning must substantially ease the scarcity of zoned units and, for this to happen, upzoning must be applied at sufficient scale vis-a-vis the relevant housing market.

The expensive coastal cities have no shortage of land per se, but of zoned units. Such units can be thought of as slots for households to stake a claim in a location, or call it home, allowing them to live in the area and access its job market. It is these slots whose scarcity is drawing a premium in the expensive coastal metros, reflected by inflated land values, whereas land per se is not in short supply. The San Francisco Bay Area, for example, whose shortage of zoned units is most acute, spanned 1,386 square miles as of 2010 and housed about 8 million people. That is enough land to house 75 or 100 million people at the average densities of Paris or Manhattan, respectively, leaving plenty of space for more moderate scenarios (see here for Paris and here for Manhattan).

When home values detach from construction costs the timing of land acquisition becomes crucial and, even then, the cost of construction still matters

Even though home values in the expensive coastal cities have diverged from the cost of construction, construction costs still matter, even there. The reason is that because developers must confront the cost of land acquisition, high construction costs can still be pivotal with respect to the viability of new construction projects. Developers only undertake projects they expect to turn a profit and, when projects are marginally profitable, every expense can be pivotal. Thus, when construction costs change they can impact profits and tip the financial feasibility of the project and, as a result, fluctuating construction costs can still influence the supply of housing in the expensive coastal cities despite being small compared to home values. The same is true of any other cost associated with producing housing including, ironically, fees and requirements imposed in the name of affordable housing.

The cost of land acquisition can be pivotal, too – especially when it is as high as it is in the expensive coastal cities – and its timing vis-a-vis the housing cycle can be crucial. Unlike construction costs, whose fluctuations over the housing cycle are relatively modest, the cost of land fluctuates with volatility that exceeds that of housing itself. Acquiring land sufficiently early with respect to the upswing of the housing cycle can make all the difference with respect to a project’s viability.

The bottom line

The disparity between the appearance of homes and their price tags is more than a home buyer’s gripe: it is a telltale indication of restricted housing supply. Such restrictions – rules governing land use, installed by incumbent residents or their predecessors – are exclusionary by nature and amount to the gating of access to opportunity. Hopefully, this study has helped identify where gates must be opened.

Data and Methodology:

1. Overview

Average home values are drawn from the 2011-2015 5-year American Community Survey (ACS) at both the metropolitan and zip code levels, and are updated to 2016 values using housing price indices from the Federal Housing Finance Agency (FHFA).

At the metropolitan level (CBSA): (i) average construction costs per home within structure size categories are inferred from the Census Building Permit Survey; (ii) average replacement costs per home are obtained as an average of the corresponding construction costs, weighted by the mix of existing structure sizes; (iii) improvement values per home are obtained based on depreciating the replacement cost based on the mix of existing structure age, assuming 1.5 percent annual depreciation up to a 30 year cap; (iv) average land values per home are taken as the difference between average home value and average improvement value per unit.

At the zip code level (ZCTA), average unit construction costs and the measures derived from them are inferred from metropolitan unit construction costs based on estimates of their variance within metros, and assumptions on the relationship between a zip code area’s location in the metropolitan home value and construction cost distributions. Zip code level estimates are appropriate for mapping differences in measures within metro areas, but rankings of zip code areas within metros should be taken with caution. Zip code areas with extreme values – e.g. those emerging at the top of within-metro rankings – are those most likely to be driven by assumptions that are broadly appropriate, but that can mischaracterize specific locations.

2. Average home values

Average home values are obtained from the 2011-2015 5-year ACS by taking the ratio of the aggregate value of owner-occupied homes and the number of owner-occupied homes in every CBSA and ZCTA (Tables B25080 and B25032, respectively). Because the values correspond to the years 2011 to 2015, they are updated to reflect 2016 values. The update was performed using the 2016 and average 2011-2015 values of the corresponding CBSA and ZCTA housing price indices (HPIs) obtained from the FHFA – see Bogin, Alexander, William Doerner and William Larson, “Local House Price Dynamics: New Indices and Stylized Facts,” FHFA Working Paper 16-01, 2016.

In some instances, the FHFA lacks HPIs for certain zip code areas. Wherever possible, the change in the ZCTA HPI was imputed from neighboring ZCTAs. Imputed values are out-of-sample predictions from a linear regression of ZCTAs’ change in HPI on a quartic polynomial of the average change in the HPI of neighboring ZCTAs. For each observed ZCTA, the set of neighboring ZCTAs included the union of the 5 nearest ZCTAs and all ZCTAs up to 2 miles away, with distances taken between centroids.

3. Average construction cost per home, within structure size categories

Average construction costs per home by structure size category were obtained for CBSAs from the Census Building Permit Survey as follows. The total value of construction and the total number of permitted homes were obtained from the Census’ county-level reporting and were summed over the CBSA. The ratio of the two totals was then taken within each of the following structure size categories: (i) single-family (attached and detached), (ii) 2 unit structure, (iii) 3-4 unit structure and (iv) 5+ unit structure.

What does the value of construction reflect when it is drawn from building permit valuations? The Building Permit Survey questionnaire asks local building department officials to enter the sum of valuations as reported on building permits. The values reported on building permits are ex-ante estimates of the value of construction put in place made by parties applying for building permits – usually contractors. Such estimates are generally constrained within strict parameters defined by the building departments, tethering them to the actual cost of construction. However, because building permit values often serve as the basis for assessing fees, those estimating them have an incentive to under-report. Thus, it is likely that construction costs in this study, which reflect building permit valuations, understate actual construction costs. A separate concern is that jurisdictions may differ in their appetite or capacity for extracting a surplus from developers, which could manifest itself in exaggerated schedules that result in higher permit valuations and higher fees. Unfortunately, no broad-based source of data is available for estimating the extent of the bias. Several manual comparisons with cost estimates from the RS Means residential construction cost calculator – which contractors often use for pricing out project bids – suggest the construction cost estimates in this study are reliable as a rough gauge.

Why estimate construction costs with data from the Census Building Permit Survey rather than from RS Means? The differences in construction costs across places have two components: (i) differences in the cost of building identical structures and (ii) differences in the characteristics of the structures built. The RS Means cost calculator only addresses (i), not (ii). Thus, although RS Means information is useful for apples-to-apples comparisons of what it costs to build an identical structure in different metros, it is does not reflect differences in the nature of structures actually built in each metro, which this study wishes to capture. Of course, one could use RS Means to price out a variety of projects with different characteristics, but one would need to find external information on what projects represent the structures being built in each metro, whereas that information is implicit in the Building Permit Survey valuations. A separate reason to use the Building Permit Survey rather than RS Means is that, because it provides construction costs that are averaged out over multiple projects, it is statistically informative with respect to the distribution of construction costs within metros, whereas RS Means is not. Information on the distribution of construction costs is useful for estimating average construction costs at the ZCTA-level, which are otherwise unobservable (see below).

4. Average replacement cost per home

4.1 At the CBSA level:

The replacement cost of an existing home is the cost of building it anew at current quality standards and construction costs. Average replacement costs per home are obtained as the average construction cost across structure size categories, weighted by structure size mix of existing homes. Thus, the resulting estimate captures what it would cost to rebuild the existing housing stock, if its characteristics were typical of new residential construction observed today (within metro area and structure size category). The structure size shares of the existing housing stock are drawn from the 2015 1-year ACS (table B25127), excluding mobile home, boats, RVs, etc’. Although the ACS recognizes several structure size categories with more than 5 units per structure, the Building Permit Survey does not. Therefore, construction costs associated with the 5+ unit structure category are weighted using the summed share of all ACS structure size categories above 5 units per structure.

4.2 At the ZCTA level:

Because the Building Permit Survey does not observe ZCTAs directly, average replacement costs at the ZCTA level must be inferred. To do so, the standard deviations of replacement costs and home values are estimated within CBSAs, and it is assumed that each ZCTA’s average replacement cost deviates from the CBSA’s average replacement cost by the same number of standard deviations as its average home value deviates from the CBSA’s average home value. In other words, it is assumed that homes in more expensive ZCTAs also cost more to build, but “how much more” is determined by the different “spreads” of construction costs and home values. The procedure above is performed in logs, and is conducted separately for each structure size category. Technical details regarding the standard deviations of replacement costs and home values follow.

For each ZCTA and structure size category combination (1, 2, 3-4 and 5+ units), the deviation of its average log home value from the CBSA-category combination’s average log home value is observed directly. The deviation is expressed in terms of the average standard deviation of log home values within CBSAs for the structure size category, which is estimated from 2015 1-year ACS microdata – see Steven Ruggles, Katie Genadek, Ronald Goeken, Josiah Grover, and Matthew Sobek. Integrated Public Use Microdata Series: Version 6.0 [dataset]. Minneapolis: University of Minnesota, 2015. http://doi.org/10.18128/D010.V6.0.

The average standard deviation of log construction costs per home within CBSAs for each structure size category is estimated as follows. First, an annual county-level panel of average log construction costs per home in each structure size category is drawn from the Census Building Permit Survey for the years 1990 to 2016. Next, after controlling for a common time trend by regressing the values on a set of annual fixed effects (weighted by counties’ average annual number of units permitted), the standard deviation of the residuals within each county is obtained. Letting [latex]Y_i[/latex] denote the (temporal) variance of the residual average log construction cost for County [latex]i[/latex] and [latex]\sigma^2[/latex] denote the variance of an individual home’s residual log construction cost, [latex]Y_i[/latex] equals [latex]\sigma^2/N_i[/latex], where [latex]N_i[/latex] is the the average number of units permitted annually in the county. The value of [latex]\sigma[/latex] is elicited from the regression [latex]\log(Y_i) = \beta_0 + \beta_1 \cdot \log(N_i) + \epsilon_i[/latex], where [latex]\epsilon_i[/latex] is an error term, and backing out an estimate of [latex]\sigma[/latex] as [latex]\hat{\sigma} = \exp(0.5 + \hat{\beta_0})[/latex]. This procedure is performed separately for each structure size category. As should be expected, the values of [latex]\hat{\beta_1}[/latex] are always negative, reflecting the reduced variance of the county average construction costs when they aggregate greater numbers of projects (the Law of Large Numbers in action!). Observations are omitted from the regressions when they have fewer than 25 structures in the corresponding size category on average per year. For the 1, 2, 3-4 and 5+ unit per structure categories the threshold is set at 25, 50, 87.5 and 250 annual units, respectively (thus, the average number of units in 5+ unit structures is taken to be 10, which is likely an underestimate).

5. Average improvement value per home

Average improvement values per home are obtained by depreciating the average replacement cost at a constant annual rate of 1.5 percent until they are 30 years old, and leaving it constant thereafter. The age of homes is observed using the year of construction categories available in the 2011-2015 5-year ACS (Table B25127).

The decrease in residential structures’ value can vary greatly, depending on a host of factors that include the nature of the structure, its maintenance, and the market environment. The academic literature estimating the rate of residential depreciation is also varied in its techniques, data sources and resulting estimates. A useful summary is provided in Francke, M. K. and van de Minne, A. M. (2017), Land, Structure and Depreciation. Real Estate Economics, 45: 415–451. The 1.5 percent annual depreciation rate is a ballpark figure that is roughly in line with past estimates.

According to Francke and van de Minne (2017), homes that are hardly maintained lose value fairly quickly, whereas homes that are well maintained hardly lose value at all. If so, the actual rate of depreciation is likely to vary substantially across places. Inasmuch as homes are better maintained in areas with greater home values, this study may be underestimating (overestimating) improvement (land) values in such areas and vice versa. However, note that this potential bias does not affect the home value to replacement cost ratio, as this ratio is independent of the depreciation rate assumption.

Depreciation is capped at 30 years because once homes hit a certain age, they are typically either torn down or undergo substantial renovation which greatly or even fully mitigates past depreciation. The timing of such major renovation can vary greatly. The 30 year cap reflects an assumption that among homes built 30 years ago or more, a subset have undergone major renovation, and the share that has undergone major renovation is such that, on average, these homes’ state of repair is equivalent to that of a 30 year old home without major renovation.

6. Average land value per home

The average land value per home is obtained by subtracting the average improvement value per home from the average home value.

Note that, inasmuch as building permit valuations underestimate actual construction costs, and inasmuch as the average value of owner-occupied homes exceeds the average value of homes drawn from the entire housing stock, this study underestimates replacement costs and improvement values and overestimates land values.

7. The home value to replacement cost ratio vs alternative measures

This presentation of this study highlights the home value to replacement cost ratio. An alternative measure that also illustrates the disparity between a home’s appearance and its price tag is the land fraction of home value, i.e. the share of a home’s value that is attributable to land. There are three advantages to the home value to replacement cost ratio. First, without additional information, high land value fractions can be interpreted ambiguously, reflecting either soaring land values or a very dilapidated housing stock. The home value to replacement cost ratio solves this by substituting replacement cost for improvement value. One cannot do so for the land value fraction – because it won’t remain a fraction – unless one also substitutes home values with “new-construction-equivalent home values,” i.e. the sum of replacement cost and land value which reflects a home’s value if it were in mint condition. However, the new-construction-equivalent home value is less intuitive and, through the land value component, it depends on the depreciation rate assumption. The second advantage of the home value to replacement cost ratio is that it is independent of the depreciation rate assumption. Finally, home value to replacement cost ratio increases linearly with land values, whereas soaring values are reflected in ever smaller increases in the land value fraction as it tends towards one.

8. Vertical vs horizontal multifamily structures

Multifamily structures can be built with a variety of construction techniques whose costs can vary greatly. A low-lying wood-framed structure is less costly to build than an equal-area steel and glass skyscraper and, more generally, once structures rise beyond a certain height or require elevator shafts or parking structures, for example, they tend to require more costly construction materials and methods.

The data used for this study does not distinguish between so-called “vertical” or “horizontal” multifamily structures. As a result, the ZCTA-level replacement cost estimates are likely understate (overstate) the true values in ZCTAs in which a relatively large (small) share of multifamily structures are “vertical.” This is likely to be most notable in downtown areas that contain many tall condominium towers.